Legal matters: Improving cashflow performance

By Alistair Dunsmuir

This guidance from the National Golf Clubs’ Advisory Association looks at the issue that many golf clubs have failed because of poor cashflow management rather than lack of profits. What can managers do to improve this vital aspect of their work?

Why do we need to bother about cashflow forecasting and what is cashflow forecasting anyway? The saying ‘cash is king’ is often used to explain the failure of businesses. Without the proper amount of cash on hand, entities can run into major trouble, and even be forced into bankruptcy. Therefore cash is the single most important financial factor in your golf club.

Cashflow forecasting is about predicting when money will move in and out of your bank account in the future. The amount of cash you have in your bank account dictates what you can and cannot do. Say it’s the end of the month and you need to pay your employees, tax, VAT or anything else. It doesn’t matter how much money you are owed; either you have the cash to pay, or you don’t.

The needs of a golf club constantly change and a good cashflow will provide details of actual cash required by your golf club on a day-today, month-to-month and year-to-year basis. Using a cashflow will highlight in advance any shortfalls in cash that need to be bridged. There are many well-documented cases of golf clubs failing not because they weren’t profitable but due to poor cashflow management.

Cashflow forecasting sounds daunting, but it is actually a deceptively simple process that effectively amounts to using available information to predict how much money you will have coming in and out of your business at any given point. Planning and managing your cash is the backbone of any successful golf club.

The most basic form of cashflow forecasting is a simple spreadsheet listing income and costs on a monthly basis. However, this can be as detailed as you require. There are also various accounting software packages available that will help you with cashflow forecasting.

Be realistic

A cashflow forecast will not be beneficial if you are not sensible when predicting income and expenses.

Income (Receipts)

- How many members does the club currently have? Is this expected to remain consistent / fall / increase? Think about if the club has any future special offers or marketing events which will increase membership. What is the annual membership fee? When are the membership fees received? (Remember an invoice to a member is not cash until it is paid).

- Does the club receive any other income? Function room rental, food, beverages, bank interest and so on. Include all sources of income.

Expenses (Outgoings)

- Include absolutely everything in your forecast, incidental expenses can add up. If you’re sailing close to the wind financially, those unplanned expenses are what tip you over the edge. If in doubt, throw it into the forecast. It’s better to have accounted for and expenses and not have to pay for it than vice versa. Expenses can be grouped to make it easier to focus on so for example

- Couse upkeep (fertilisers, machine repairs, sprinklers and so on.)

- Staff costs (management and administration, course upkeep and maintenance, clubhouse bar, clubhouse catering and so on.) Remember to consider auto enrolment of staff on to pensions if your club staging date is coming up for those of you that are already auto enrolled remember to factor in any changes in employer pension costs as the percentages rise.

- When you separate your costs into different categories, take some time to think about which are fixed and which are variable. Things like rental of equipment, rates, broadband and so on are likely to remain the same the whole year, which makes forecasting easier. Other costs may vary, think about what you have going on at your club, if you have Christmas functions, weddings and so on then catering and beverage costs will increase. What are the terms of payment with these suppliers, on delivery, 30 days and so on? Factor these variances into your cashflow forecast.

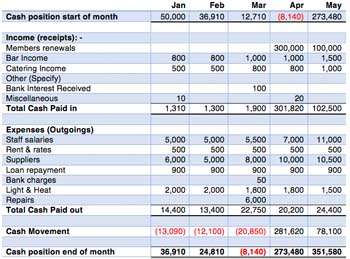

If the majority of your income happens at a particular time of the year (members’ renewals), a cashflow forecast will help you plan your expenditure (see the example) for the portion of the year when your income is lowest, and allow you time to put contingency plans in place should your cashflow look unhealthy.

From the example it can be seen that the March cash position at the end of the month is overdrawn. Therefore, for this month you may need to speak to the bank to discuss an overdraft facility, talk to suppliers to increase payment terms, try to promote early renewal of memberships and so on to bridge this shortfall in cash.

Moving document

Once you have prepared your cashflow forecast for your club, don’t just put it to one side and forget about it, in order for it to be a useful tool for your club you need to be continually updating it with actual figures. Depending on the situation in your club this may need to be on a daily or weekly basis, at the very least each month as part of your month-end management accounts procedures.

Remember you don’t want your golf club to be the one that goes bankrupt although it is profitable on paper. So start by preparing a cashflow forecast for the coming 12 months. Remember you can start by preparing a simple cashflow forecast and then over the coming months this will naturally become more detailed as you use this useful tool for your golf club. If you are thinking of developing the club and this requires major funding this tool will help demonstrate that you have thought about how the club is going to acquire the funds or if it requires a lender then they can see that you have thought about loan repayments and can demonstrate that the club can make the repayments as they fall due.

Happy forecasting!

Jackie Howe, the chief executive, is based in the office and is on-hand to offer advice and support. She is backed up by a team of specialist Solicitors to assist in legislative guidance for clubs.

The National Golf Clubs’ Advisory Association

The Threshing Barn, Homme Castle Barns,

Shelsley Walsh, Worcestershire, WR6 6RR

Tel: 01886 812943

email info@ngcaa.co.uk

By Alistair Dunsmuir

Write a comment

3 Comments

View comments

Write a comment

|

|

|

|

|

|

Yes, I think that it is very important to be always relialistic. I think that Cashflow forecasting is definitely helpful.

I feel the real value from watching cashflow will come from my experience.

As so often the case such articles are written from a private members club perspective rather than a proprietor’s : and very few in golf understand the difference. Dare I say you have to be a proprietor to really understand the difference.

Jackie’s article assumes the Secretary/manager has the luxury of being able to borrow (and pay the resultant interest) from a bank or to fall back on 300 members : “We need cash! Pay £30 each or we go under”

In my experience, that position often makes Private members clubs very wasteful and inefficient. As with many other proprietors, I listen politely to dinner table conversations whilst thinking

“If you did that here you would go out of business very fast” I could give loads of examples but fear of offending tells me to keep quiet.

Similarly, when someone takes over a failing club and the magazines get all excited about the resulting leap in new machinery and staffing levels I know either the new buyer has a lot of spare cash to throw away or they will not be in business in five years time.

Many years ago I listened to an interview with Lord Wienstock (Chairman of highly successful GEC). The programme was to last 40 minutes but almost finished after 3 because his answer was so simple.

BBC Presenter: Other major industries have been the subject of mergers and takeovers yet GEC has rejected all such offers continues to grow and is now recognised as one of the most successful and stable business in the world (C1990).

Weinstock: There are always times of famine and times of feast, more famine than feast.In times of feast, we store up enough cash to see us through the famine. At the ned of the famine, we look around and many of our competitors have merged ,been taken over or gone bankrupt whilst we are still trading.

This is the only way a successful proprietor can operate. You will and must carry your cash flow in your head at all times. You know you cannot call on members to bail you out and it is deadly to ever pay interest to a lender-what a terrible waste of money.

Faced with this outlook I doubt very much if many private members clubs could operate at all, but would help them greatly if they were to head that way.

You carry your cash flow in your head:- never buy anything for a golf Club that you can’t afford and never put any money in that you can’t see coming back as a result.